You're Probably Planning for the Wrong Retirement Country

In 2019, I built the most complete financial model I'd ever built. Every column had a source. Every number was researched. I knew the exchange rate. I knew the cost of groceries in Koramangala. I'd even talked to a broker in Whitefield about land prices. The model said: return to Bangalore at 55, retire comfortably.

Then my daughter got into a good school district here. My father-in-law had a health scare there. My wife got a promotion she didn't want to walk away from.

None of that was in the model.

By 2021, I had quietly stopped updating the India columns. I wasn't returning. I just hadn't said that to anyone, including myself. The spreadsheet still opened to Bangalore as the base case.

Three years of retirement planning with the wrong country as the assumption. Every number was wrong. The tax projections were wrong. The healthcare estimates were wrong. The portfolio drawdown strategy was wrong. The estate structure was wrong.

This isn't a financial planning failure. It's an identity planning failure that shows up as a financial planning failure.

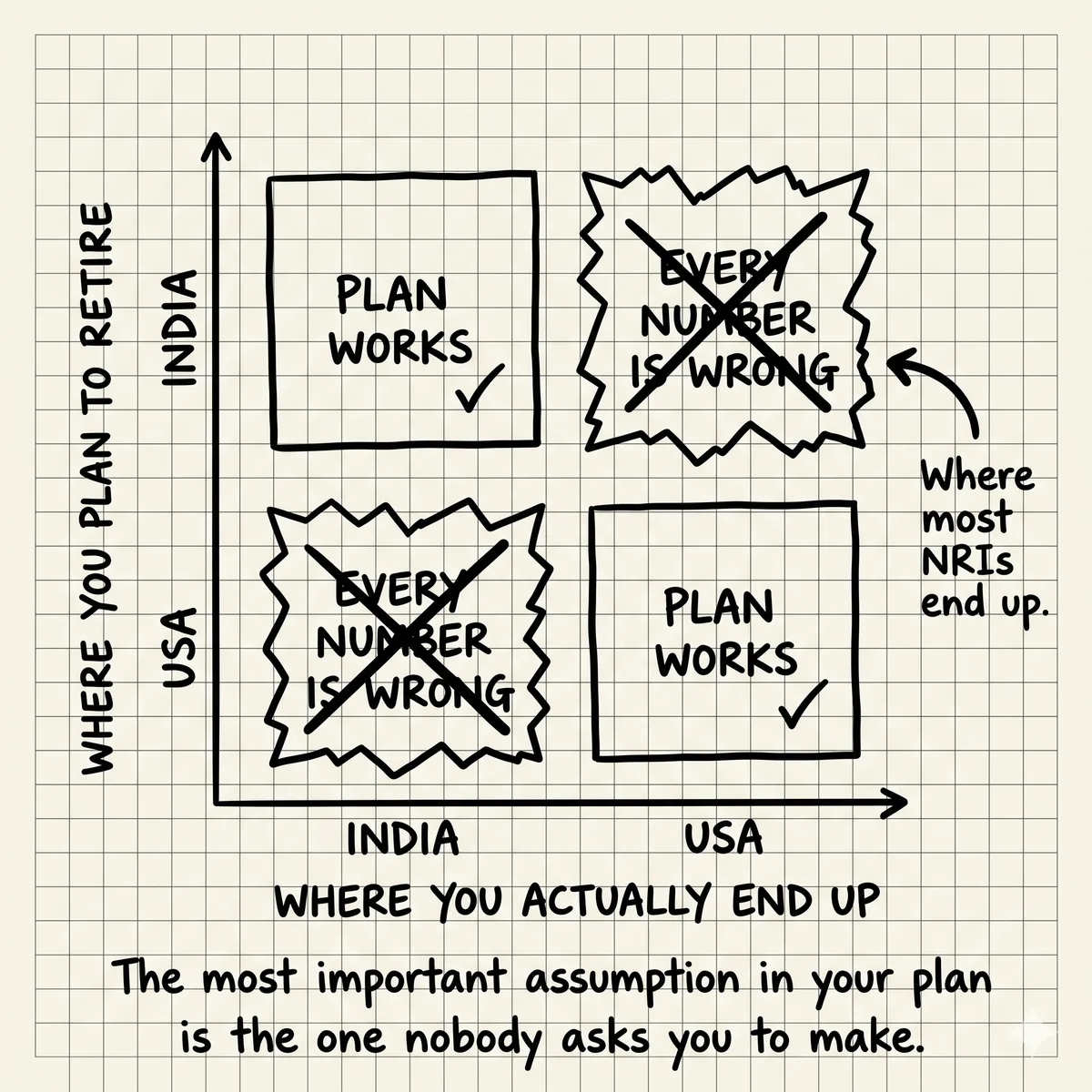

The Most Important Assumption in Your Retirement Plan

Every retirement plan rests on a location assumption. Where you'll live determines: your cost of living, your healthcare costs, your tax obligations, your portfolio size requirements, your Social Security strategy, your Medicare eligibility, your estate planning jurisdiction, and your currency exposure.

For most Americans, that assumption is baked in silently. They'll retire in the US. The plan reflects that without anyone naming it.

For an NRI, the assumption is contested and often unresolved. You moved to the US in your 20s. You built a career. You saved in USD. You have accounts, equity, real estate, and maybe family obligations on two continents. The question of where you'll retire is genuinely open, and it's been open for 15 years, and you've been deferring it.

That deferred decision is the single most expensive assumption in your financial plan. Not because the answer matters so much in itself. Because every other number depends on it, and it's unspoken.

The deferred decision is still a decision.

If you haven't decided where you're retiring, your financial plan has decided for you. Whatever country your advisor defaults to, whatever tax software assumes, whatever healthcare cost estimate uses — that's your assumed retirement location. It's probably wrong.

The Two Failure Modes

Failure Mode 1: Plan for India, Stay in the US

You built your whole plan around a lower cost of living in Bangalore. Your target portfolio size is $1.8M because that's plenty for India. You've been drawing down faster than you'd draw down for the US. You haven't enrolled in the right Medicare supplemental coverage. Your estate documents assume Indian jurisdiction for some assets.

Then you don't go. The kids are here. The grandkids are here. You're 64 and you've been in the Bay Area for 30 years and India is where your cousins live, not where you live.

You're now 64 with a $1.8M portfolio that's supposed to last 25 years in India, in the US. US healthcare alone will burn through your surplus projections in the first decade. The numbers don't work.

Failure Mode 2: Plan for the US, Return to India

You've been maxing your 401(k), building Social Security credits, contributing to a Roth. Your portfolio is $2.8M, all in US-domiciled accounts. You have Social Security coming.

Then you return to India. Your US retirement accounts now have India tax implications that your US advisor didn't model. Social Security is taxable in India under DTAA rules. Your Roth distributions get treated as ordinary income by Indian tax authorities. Your estate doesn't pass cleanly under Indian succession law.

The accounts built for one country are optimized for the wrong one. Not wrong in total, but wrong in structure. The cross-border complexity of unwinding this in retirement is enormous and expensive.

What Each Plan Actually Costs

US retirement: What you actually need

- Annual spending estimate (comfortable, mid-cost metro): $90,000-$130,000

- Healthcare (pre-Medicare, age 62-65): $18,000-$28,000/year for a couple on ACA

- Medicare + supplement (post-65): $8,000-$15,000/year for a couple

- Required portfolio (4% rule, 30-year horizon): $2.25M-$3.25M

- State tax exposure: Depends heavily on state. California retirees pay income tax on IRA distributions.

India retirement: What you actually need

- Annual spending estimate (comfortable, Bangalore/Mumbai/Pune): $30,000-$55,000 (at current exchange rates)

- Healthcare (private, good coverage): $2,000-$5,000/year for a couple, but with meaningful quality variance

- Required portfolio (4% rule, 30-year horizon): $750K-$1.375M

- Tax exposure on US account distributions: Complicated. Roth distributions taxable as ordinary income. 401(k) distributions taxable. DTAA applies but imperfectly.

- Currency risk: You hold USD assets, spend in INR. A 10% rupee depreciation increases your effective cost of living by the same amount.

The gap between these two numbers is roughly $1M to $1.9M in required portfolio. If you've been planning for India but will stay in the US, you're $1M to $1.9M short of where you need to be. That's not a rounding error.

Healthcare: The Variable That Dominates

US healthcare is the single biggest reason to run both scenarios. The difference between US and India healthcare costs in retirement is $500K to $1M in lifetime spending for a healthy couple, and the variance explodes with any serious illness.

In India, a good private hospital is genuinely world-class for procedures that would cost $150K in the US and cost $8K there. Major surgery, oncology, cardiac events — the per-procedure cost difference is dramatic.

But India also has gaps: chronic disease management, mental health care, rare conditions, the logistical challenge of being far from your US-trained doctors, and the very real possibility that at 78 you don't want to be navigating a complex health situation 9,000 miles from where your kids live.

The healthcare planning horizon for cross-border families is not "where's the cheapest care." It's "where do I want to be sick, and what does that cost?" That's a different question.

Most retirement plans for NRIs ignore this entirely. They pick one country's healthcare cost and model it straight to 85. The real plan accounts for the possibility of healthcare decisions driving your residency choice in ways you can't fully predict at 45.

Three Questions That Actually Clarify This

Not "where do you want to retire?" That's too abstract and too easily answered with what sounds good rather than what's real.

These three questions cut through the abstraction:

Question 1: Where will your adult children live?

Not where they are now. Where they'll be in 15 years. Most NRI parents who say "we'll retire in India" have adult children who are either US citizens already or very likely to become US citizens. In 15 years, the pull of grandchildren changes the retirement country calculation for most people more than any financial analysis does.

Question 2: What does "not being well" look like at 75?

Retire in India and get a major health event at 75. Walk through that scenario in detail. Who do you call? What hospital do you go to? Who manages your care? Who's in the room? The answer to that question tells you more about your real retirement country than any cost-of-living comparison.

Question 3: Have you spent 30+ consecutive days in India in the last 5 years?

Not a vacation. An extended stay. If you haven't done this, your India retirement plan is based on your memory of India from 15 years ago, not the India that exists now. The city has changed. Your social network there has changed. Your parents who anchored the India plan aren't young anymore. This is the most underestimated variable in the whole decision.

The right plan models both countries simultaneously

The answer isn't to pick a country and plan for it. The answer is to maintain two live models, know exactly what it costs to pivot from one to the other, and update both models every year as the decision gets clearer.

Most financial tools can't do this. They're built for people who know where they're retiring. The peer data that matters comes from NRIs who faced this exact decision and landed somewhere — their real outcomes, not theoretical models.

What the Peer Data Looks Like

The NRIs who navigate this well have one thing in common: they made the "where" decision explicitly, updated it as life changed, and built a plan that reflected the actual decision rather than the wished-for one.

Some of them decided early: "We're staying. India is for visits." They built US-optimized accounts, bought in the Bay Area, structured their estate for US law. Clean decision, clean plan.

Others decided equally explicitly: "We're going back at 58. Kids are on their own." They structured their savings for RNOR optimization, kept Indian real estate in their own names, held some assets in India. Clean decision, different plan.

The most financially damaged cohort is the one that kept both options open indefinitely, optimized for neither country, and ended up with a mismatched set of accounts and obligations at 62 with no clean path forward.

The geography arbitrage opportunity is real, but it only works when you've made the decision explicitly. Arbitraging two countries requires committing to one as your tax home and treating the other as a strategic asset. Keeping both ambiguous doesn't give you the best of both worlds. It gives you the tax complexity of both and the planning benefit of neither.

I updated my spreadsheet. The India columns are still there. But now they're clearly labeled "scenario B" and there's a column that says "decision date." The decision date is blank. But at least now the plan knows the decision hasn't been made. That's more honest than the version that silently assumed Bangalore was settled.

A plan that knows it has an open assumption is better than a plan that thinks all the assumptions are settled.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

You're Making $400K and You Still Don't Feel Wealthy. Here's Why the Benchmark Is Wrong, Not You.

Priya earns $420K in San Francisco, has $800K saved, and feels behind. She's comparing herself to HENRYfinance posters who have no parents to support, no cross-border obligations, no Bay Area cost structure. The benchmark is wrong, not her.

Your FIRE Spreadsheet Doesn't Work When Your Assets Live in Three Countries

The spreadsheet was elegant until you added the EPF tab. Then the Bangalore apartment. Then the RSUs. Then exchange rates. Then two retirement countries. It broke somewhere around column AK — and that's not a spreadsheet problem.

180-Day Window: Critical Steps After Liquidity Event

After exit or IPO, 6 months determine everything: over-concentration, tax errors, lifestyle lock-in, estate planning failures. Sequence the right decisions before permanent lock-in.