Your Wealth Is 30% Smaller Than You Think

Vinay slid a napkin across the table. "That's not your number," he said. "That's your pretax number. These are different things."

We were at dinner. Vinay Sambamurthy has spent 20 years as a financial planner. He works with people who have between $1M and $10M in investable assets. He's seen the same conversation so many times he can script both sides.

"I had a client last month," he said. "Sat down with me and said, I have $3M. I'm ready to retire. I just want you to confirm the math." He paused. "The math was fine. Except the number he had wasn't $3M. Not in any sense that matters."

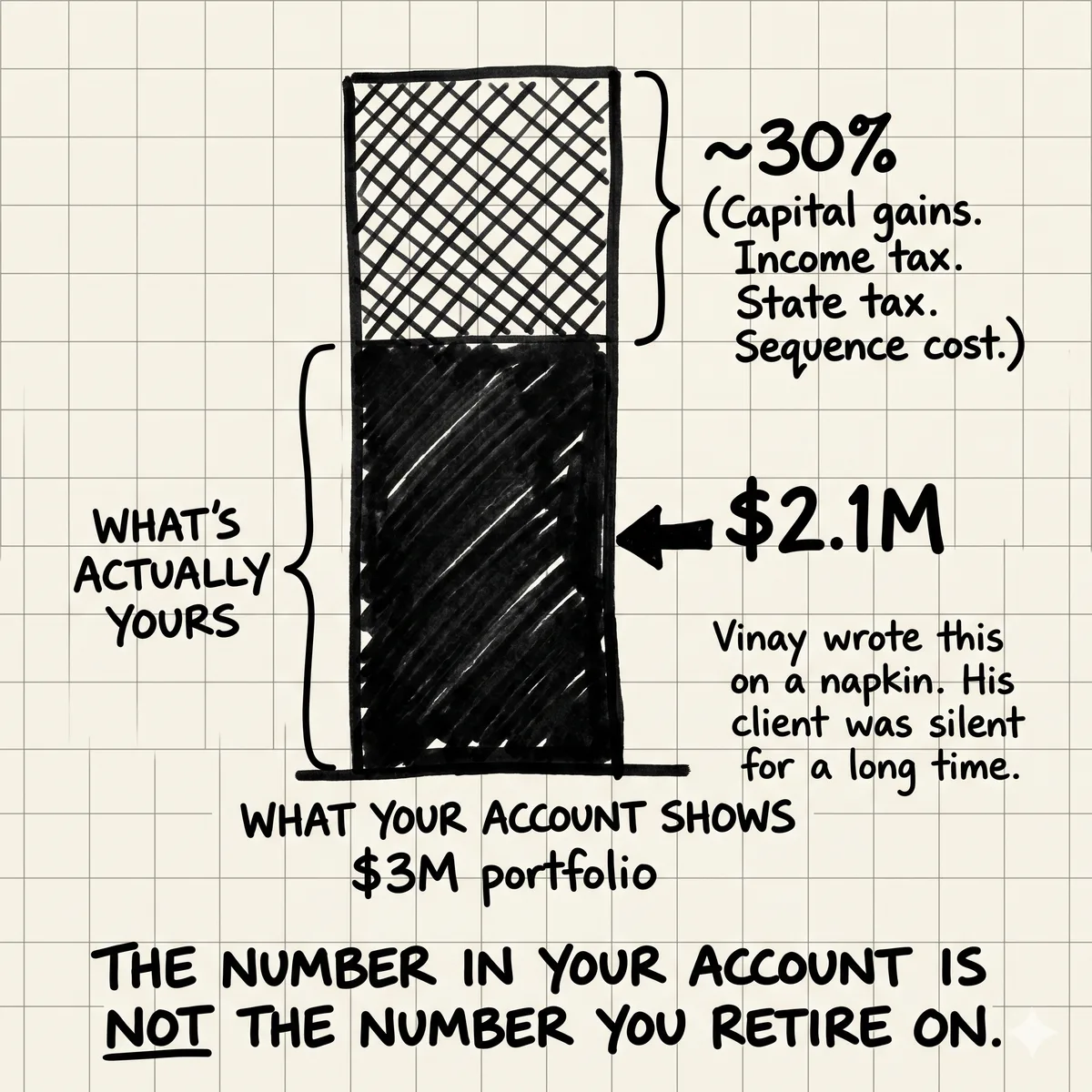

He wrote $2.1M on the napkin.

"That's what's left after he actually retires," Vinay said. "The $3M is what he sees in his accounts. The $2.1M is what he can spend. He was planning for $3M. He has $2.1M. He's not in trouble. But he's 30% away from where he thinks he is."

That 30% is not a rough estimate. It's where the money goes if you don't plan around it.

Where the 30% Goes

The gap between the number in your accounts and the number that's actually yours isn't random. It comes from specific, predictable sources.

Capital Gains Tax on Your Taxable Brokerage

If you have $800K in a taxable brokerage account and you've held those positions for years, a significant portion of that balance is unrealized gains. When you sell to fund retirement, you'll pay capital gains tax on those gains. Long-term capital gains rates are 0%, 15%, or 20% at the federal level, plus state tax if you're in California, New York, or Massachusetts.

At $250K in retirement income, you're looking at the 15% federal bracket for most gains, plus 9.3% in California. That's 24.3% of gains going to taxes. On an account where 60% of the value is gains, you're losing 14.6% of the account value to taxes on liquidation. Not on every dollar. But on the gains dollars.

Ordinary Income Tax on Traditional 401(k) Distributions

Every dollar you pull out of a traditional 401(k) or IRA is taxed as ordinary income. Not at capital gains rates. At income tax rates. For most people in early retirement with meaningful distributions, that means effective rates of 22-32% federal plus state.

If your retirement income plan involves $100K annual distributions from a traditional 401(k), you're netting $68-78K after federal tax and losing more to state. The $1.2M you see in the account statement is worth somewhere around $840-900K in actual spendable money. That's the number that funds your life.

Required Minimum Distributions Push You Into Higher Brackets

Traditional 401(k)s and IRAs require distributions starting at age 73. The RMD formula forces increasingly large withdrawals regardless of whether you need the money. If you haven't done Roth conversions during your early retirement years when your income is lower, you'll be forced to take large taxable distributions later, often pushing you into higher brackets and increasing your Medicare premium surcharges (IRMAA).

State Tax Varies Dramatically

California taxes capital gains as ordinary income. That's up to 13.3% on top of federal. If you retire in California with a $3M portfolio and $1.5M of it in taxable accounts with significant embedded gains, you're paying substantially more than someone in Texas or Florida with the same portfolio. State of retirement matters. Most retirement plans don't model this explicitly.

The Four Accounts and Their Real After-Tax Value

Taxable Brokerage

What you see: $800K. What's yours: depends on cost basis.

If cost basis is $400K (50% gains), you owe tax on $400K of gains. At 24.3% combined rate (15% federal + 9.3% CA), that's $97K in taxes. After-tax value: approximately $703K. That's 88% of the stated value. The percentage gets worse as gains grow larger relative to cost basis.

Traditional 401(k) / IRA

What you see: $1.2M. What's yours: roughly $840-900K.

Every dollar is taxed as ordinary income on distribution. At a blended 28-30% effective rate on distributions, $1.2M nets approximately $840-864K. Some states tax retirement distributions; some don't. The RMD risk can push this number lower if you're forced into higher brackets.

Roth IRA / Roth 401(k)

What you see: $400K. What's yours: $400K.

Qualified distributions are tax-free. This is the full-value account. It's also the one most people have the least of relative to their traditional accounts, because they contributed to traditional accounts for the upfront deduction during their high-earning years.

HSA

What you see: $80K. What's yours: $80K (if used for healthcare) or ~$56K (if used for non-healthcare after 65).

The HSA is the triple-tax-advantaged account. Tax-free contributions, tax-free growth, tax-free withdrawals for qualified medical expenses. If your healthcare costs in retirement are significant (they will be), the HSA is actually worth more than face value as a retirement asset. Most people have far less in their HSA than they could.

The blended after-tax value of a $3M portfolio with a typical allocation across these account types comes out to roughly $2.1-2.3M in actual spendable money. That's Vinay's napkin number. And it's not a pessimistic estimate. It's the math.

The Liquidation Sequence Problem

Most people will pay more than 30% because they'll liquidate in the wrong order.

The typical instinct is to liquidate in order of account size or convenience. Or to let the financial advisor decide. Or to just pull from wherever the money is when you need it.

The right liquidation sequence is calibrated to your marginal tax bracket in each year of retirement. In early retirement, when your income drops from $400K to, say, $80K in distributions, your marginal rate drops dramatically. That's the window to do Roth conversions. Pull from the traditional 401(k) up to the top of the 22% bracket. Convert the rest to Roth. Pay tax at 22% now instead of 32% later when RMDs force your hand.

The cost of wrong sequencing

A person who doesn't do Roth conversions in their 60s and gets hit with large RMDs at 73 can easily pay $80-120K more in lifetime taxes than someone with the same portfolio who sequenced correctly. Wrong sequencing doesn't just cost you money. It amplifies IRMAA (Medicare premium surcharges), increases your Social Security taxation, and reduces your estate's value. The correct sequence is worth modeling explicitly, not leaving to default.

Portfolio Value vs. Retirement Wealth

These are different numbers. Most people conflate them. The conflation is harmless while you're accumulating. It becomes expensive when you're planning for retirement.

Portfolio value is what you see in your account statements. It's the number your advisor shows you in the quarterly report. It's what you tell people at dinner when the conversation turns to finance. It's the number that makes you feel prepared.

Retirement wealth is what you can actually spend. It's the after-tax, after-liquidation, sequence-optimized number that funds your life from the day you stop working until the day you die. It's smaller. It's the number that matters.

The HENRY tax stack post covers the structure of tax optimization for high earners. The insight there is the same: the tax drag is larger than people expect, and most of it is preventable with the right architecture.

The Number That Matters

Stop planning for the number in your accounts. Start planning for the number that's actually yours. They're not the same. The gap between them is your tax bill in retirement. It's 100% controllable if you plan around it now.

What Optimizing for the After-Tax Number Looks Like

There are four moves that directly reduce the gap between your portfolio value and your retirement wealth.

1. Account Type Strategy During Accumulation

Max the Roth IRA while you can (income limits at $161K for single, $240K for married filing jointly in 2026). Use backdoor Roth if you're over the income limit. Max the HSA and invest it. Use the mega backdoor Roth if your 401(k) plan allows after-tax contributions with in-plan Roth conversion. Every dollar you get into Roth now is a dollar you can spend tax-free in retirement.

2. Roth Conversions in the Early Retirement Window

The 5-10 years between early retirement and when Social Security and RMDs kick in is a tax valley. Your income is lower. Your bracket is lower. That's the window to convert traditional IRA/401(k) balances to Roth, paying tax at the lower rate. This reduces future RMDs, lowers your lifetime tax bill, and increases the after-tax value of your estate.

3. Capital Gains Harvesting vs. Tax-Loss Harvesting

Most people know about tax-loss harvesting (selling losers to offset gains). Fewer people know about intentional capital gains harvesting in low-income years. If your income in a given year is below the 0% capital gains threshold ($47,025 for single in 2026, $94,050 for married filing jointly), you can realize capital gains at 0% federal rate. That's an opportunity to reset your cost basis in taxable accounts, reducing future tax liability.

4. Asset Location

Where you hold different asset types matters as much as what you hold. Bonds and REITs generate ordinary income. They belong in tax-advantaged accounts. Growth equities that you plan to hold long-term belong in taxable accounts (where you get capital gains treatment at sale). High-turnover funds belong in tax-advantaged accounts. Getting asset location right can add 0.5-1% per year in after-tax returns without changing your investment strategy at all.

The Cross-Border Tax Layer

For NRIs, the after-tax number gets more complicated. The DTAA between the US and India covers many income types, but the interaction between Indian capital gains rules and US tax treatment creates gaps that most tax preparers miss.

If you have Indian mutual funds or equity holdings, the Indian capital gains rules apply on the Indian side. Short-term gains (held less than 12 months) are taxed at 20% in India now (post-2024 budget changes). Long-term gains above 1.25 lakh are taxed at 12.5%. You also owe US tax on those gains as a US resident. The foreign tax credit partially offsets the double taxation, but the interaction is complex enough that the net after-tax number is rarely what people expect.

The transition year tax map covers the specific sequences that matter when you're managing assets across both countries. The days you spend in India, the accounts you draw from, and the order in which you realize income all interact with your residency status in ways that affect your total tax bill by thousands of dollars.

And for people approaching residency change, the 180-day window is one of the most specific and actionable planning moments in the entire cross-border financial picture.

What Peer Data Shows

Most people reaching retirement age with $3M in assets have never seen a clean comparison of what people with similar portfolios actually netted in retirement. Advisors don't share that data. Tax software doesn't model it. Retirement calculators show you a number that assumes a static tax rate.

What NettWorth's founding cohort is building is exactly this: the actual after-tax retirement numbers for people with complex portfolios. Not what the calculator says. What people with your specific mix of account types, your state of residence, your equity comp history, and your cross-border assets actually ended up with.

Vinay's napkin number isn't bad news. It's accurate news. The person who knows the real number can plan around it. The person who's planning for $3M when they actually have $2.1M is going to find out the hard way, and probably at a moment when there's not much left to do about it.

Your wealth is 30% smaller than you think. That's fixable. But only if you start planning for the real number.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Your EPF Balance Is Probably Taxable in the US. Nobody Told You.

The IRS has not issued clear guidance classifying EPF as a qualified pension plan. The conservative position: interest accruing annually in your EPF is US-taxable income, even if you haven't withdrawn a rupee. Most NRIs in the US have never reported it.

Roth IRA Is a Tax Trap for NRIs Returning to India

India taxes Roth distributions as ordinary income. The account everyone told you to max is built for a US retirement, not an India return. Most NRIs find this out too late.

You Inherited a Brokerage Account. Here's What 'Basis Step-Up' Actually Means.

When you inherit a brokerage account, the cost basis resets to the date-of-death value — meaning decades of capital gains can simply disappear as a tax liability. Most inheritors don't find out until after they've already sold.