What Your Financial Adviser Refuses to Show You

Robert asked the question at the end of an annual review meeting. His adviser changed the subject. Robert asked again the next quarter. Different subject again. That's when Robert understood: this wasn't an oversight.

Robert has worked with the same financial adviser for 25 years. He's 58. His adviser has managed the relationship through two market crashes, a job change, a divorce, and three different cities. Robert trusts the man. He'd recommend him without hesitation.

He has $4.2M with the adviser. Mostly in a managed portfolio of diversified funds, some individual securities, some alternative allocations added in the last decade. The relationship has been good.

At the end of an annual review last year, Robert asked a simple question. "How have my returns compared to clients similar to me? Other people your age, with roughly the same risk profile, similar time horizon?"

The adviser said: "Returns vary a lot based on individual circumstances. It's hard to make direct comparisons." He moved to the next slide.

Robert asked again at the next quarterly call. This time more specifically. "Among your clients with $3-5M in assets, similar allocation to mine, how have I done over the last ten years relative to the median?"

"I'm not really able to share information about other clients," the adviser said. Different subject. Portfolio review. Estate planning update.

Then Robert realized: the adviser doesn't want that conversation. Not because the performance is bad. Because the comparison would raise questions the adviser can't answer profitably.

What Your Adviser Will Show You

To be fair to advisers, there's a lot they do show you. The information they provide is genuine and often useful.

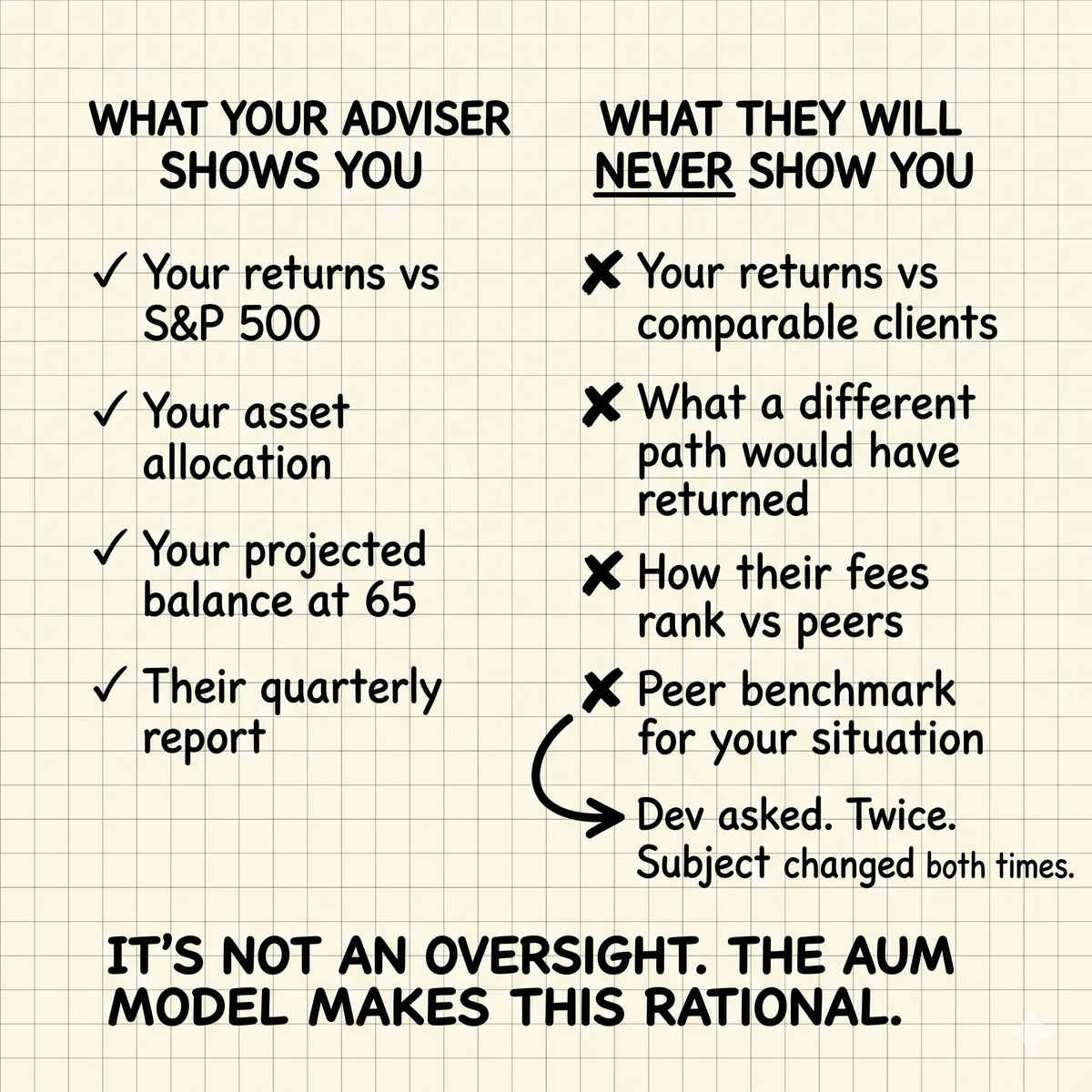

They'll show you your portfolio performance against market benchmarks. Usually the S&P 500, sometimes a blended benchmark matched to your allocation. The performance report will show you 1-year, 3-year, 5-year, and 10-year returns. If you're underperforming the benchmark, you'll see that clearly. Most advisers who use this comparison are confident they can defend it.

They'll show you your portfolio allocation. What percentage is in equities, fixed income, alternatives, cash. They'll show you whether you're within the target ranges you agreed on at the start. They'll rebalance to maintain those ranges. That's a real service.

They'll show you projections. Monte Carlo simulations showing probability of success for your retirement plan under different market scenarios. The output is usually something like "87% probability of not running out of money over 30 years." These are sophisticated models based on real data.

They'll show you tax-loss harvesting activity, estate planning updates, insurance coverage recommendations. The planning work is real.

All of this is about your portfolio in isolation. Not about how your portfolio compares to anyone else's.

What Your Adviser Won't Show You

The three things advisers almost never show clients are the three things that would actually help clients evaluate the relationship.

1. Peer Performance Comparison

How have you done compared to clients in your peer group? Not compared to an index. Not compared to "the market." Compared to people who were in your same approximate financial situation, working with advisers (possibly the same adviser, possibly others), making similar decisions over the same time period.

This is the most useful comparison you could have. An S&P 500 benchmark comparison tells you how your managed portfolio did against passive indexing. That's valuable but it's not the whole picture. A peer comparison tells you whether the specific advice you received — the specific allocations, the specific rebalancing decisions, the specific tax strategies — added value compared to what comparable clients experienced.

No adviser will ever show you this. Not because the data doesn't exist (advisers have it, or could compile it). Because showing it creates a comparison that the adviser would have to explain and defend. If you're in the bottom quartile of their clients over 10 years, what's the explanation? If you're in the top quartile, the adviser might show you. They won't show you if the comparison is neutral or unfavorable.

2. Fee Benchmarking

Most advisers charge AUM fees. The standard is 1% annually on assets under management. On $4.2M, that's $42,000 per year. At 0.75%, it's $31,500. At 0.5%, it's $21,000.

Robert's adviser charges 0.85%. Is that competitive? Robert doesn't know. His adviser has never shown him where 0.85% sits relative to what other advisers charge for a similar service and asset level. A sophisticated fee benchmarking conversation would show: here are the ranges charged by advisers at this AUM level, here's where my fee sits, here's what justifies the premium (or discount) relative to alternatives.

That conversation never happens. Not because advisers don't know the market rate for their services. Because fee comparisons create negotiation pressure and shopping behavior.

The compounding cost of 0.3%

A 0.3% fee difference on $4.2M over 20 years, assuming 7% annual returns, costs approximately $340,000 in additional fees plus foregone growth. That's not a rounding error. That's a real number that a client would absolutely care about if they saw it. The adviser's incentive is to not make this calculation visible.

3. Counterfactual Modeling

What would Robert have if he'd done something different? Not different adviser. Different structure entirely. If Robert had put $4.2M in a three-fund index portfolio 10 years ago and paid 0.05% in fund fees instead of 0.85% in adviser fees, where would the portfolio be today?

That calculation is specific and knowable. The S&P 500 returned 12.7% annually over the last 10 years. A simple Vanguard three-fund portfolio with a 70/30 equity/bond split returned something in the 9-10% range. With 0.85% fees, Robert's net return was 0.85% lower each year than it otherwise would have been. Over 10 years on $2M starting balance, that fee drag compounds to a real number.

No adviser will ever show you this comparison. Not because it's impossible to model. Because it's the question the entire AUM model depends on not being asked.

Why the Incentive Structure Makes This Rational

Robert's adviser isn't doing anything wrong. He's operating rationally within a fee structure that makes transparency about peer comparison actively harmful to his business.

The AUM model charges a percentage of assets. The adviser's revenue grows as the client's portfolio grows. The adviser's revenue depends on keeping the client. A client who does a peer comparison and sees they're underperforming other clients is a client who shops around, renegotiates fees, or moves to a passive strategy. All of those outcomes reduce the adviser's revenue.

The rational response for the adviser is to provide excellent service, strong projections, and clear performance data — while never creating the comparison that would trigger client churn. This isn't malicious. It's how every rational actor in an AUM structure behaves.

The fundamental problem is that the adviser's incentive is to manage assets. The client's need is to understand whether the approach is optimal for their situation. These aren't always the same objective.

The Information Gap

The adviser manages your assets. Nobody is managing the comparison between your outcomes and what was possible. That gap is where wealth leaks. It's not malpractice. It's structure. The structure points away from the comparison you most need.

What "Financial Transparency" Actually Means

The financial industry talks a lot about fiduciary duty, transparency, and client-first advice. Fiduciary advisers are legally required to act in the client's best interest. That standard is real.

But fiduciary duty doesn't require showing clients how they compare to their peers. It requires not putting the adviser's interests above the client's. These are different standards. You can be a fiduciary and still never show your client a peer comparison.

True financial transparency would mean: here's how you've done relative to comparable clients, here's what this relationship costs you relative to alternatives, here's what a different allocation or fee structure would have produced. Nobody in the industry proactively provides this.

The document problem post covers the broader issue of information that's relevant to your financial life but systematically unavailable. Peer benchmarking is the most obvious example, but it's one of many places where the information you need doesn't exist in any accessible form.

The HENRY wealth gap framework shows the pattern clearly: people at the $2-5M level are doing well by absolute standards but have no clean way to know if they're doing well relative to what was possible. That's the transparency gap.

What the Client Needs That the Adviser Won't Provide

Robert needs three pieces of information that don't exist in any report his adviser will ever generate.

First, a distribution of outcomes for people who were in his financial situation 10 and 20 years ago. Not a projection. Actual outcomes. What did people with $1M at age 38, similar income, similar risk tolerance, end up with at 58? What's the 25th percentile, median, and 75th percentile outcome? Where does he fall in that distribution?

Second, a fee comparison that shows what he's paid in total costs over the relationship and what the comparable total cost would have been on a passive, low-cost strategy. Not to switch necessarily. To understand what he's bought and whether the value is proportional to the cost.

Third, a path comparison. If he had made different decisions at specific crossroads — the 2008 crash, the 2020 dip, the decision to add alternatives in 2016 — what are the ranges of outcomes that different choices would have produced? Not to second-guess. To calibrate the quality of advice he received at key moments.

None of this information damages a good advisory relationship. If the adviser's performance is strong on peer comparison, the data confirms the value. If it's weak, the client deserves to know. Either way, the client is better informed.

There's a harder version of Robert's problem, and it belongs to anyone whose money lives in more than one country. Robert at least has one adviser who can see his whole portfolio and chooses not to benchmark it. If half your assets sit abroad, no single adviser can see the whole thing to begin with. Your US adviser benchmarks the US half against the S&P 500 and stops at the border. The accountant who handles the other half has never been shown the US accounts. The peer comparison Robert was denied assumes someone is holding the full picture and withholding it. When you're cross-border, the full picture has never been assembled by anyone except you, on a spreadsheet, late at night.

NettWorth's Angle

The peer benchmarking gap is specifically and deliberately what NettWorth is being built to fill.

The data that makes peer benchmarking possible doesn't exist in any advisory firm's system in a form they'd share with you. It exists in the aggregate experiences of people who were in your situation, made their choices, and have been living with the outcomes.

A corpus of real portfolios from real people, with real decisions logged at key moments, makes it possible to answer Robert's question honestly. Not "here's a projection for you specifically." Here's the actual distribution of what happened to people who were in your situation.

The founding cohort of NettWorth users is building that data. Not synthetic. Not fabricated. Real portfolios, real decisions, real outcomes. What the next Robert will be able to see is what no adviser will ever show him.

Robert kept working with his adviser after asking that question. He's still with him. But now he knows something his adviser doesn't want him to know: the comparison exists, even if nobody's made it visible yet.

If you want to understand where peer benchmarking fits in the broader picture of wealth intelligence, the AI knows the market post is a useful frame for thinking about what's now possible with the right data and what's still missing.

The question Robert asked isn't an unreasonable one. It's the question every client should be asking. The fact that no adviser will answer it tells you everything about whose interests the system is designed to serve.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Net Worth by Age Charts Are Wrong

The SCF benchmark is the most rigorous household wealth dataset in the US — and it doesn't count your EPF, your Hyderabad apartment, your unvested RSUs, or your NRE FDs. For cross-border HENRYs, the standard benchmark is measuring the wrong person.

Document Problem: What Your Advisor Doesn't Have

Documents your advisor doesn't see: offer letters, equity grants, insurance, leases. One missed clause costs $50K-$500K. Here's what they need to protect your wealth.

NRE, NRO, and FCNR: The Three Indian Bank Accounts That Determine Whether Your Money Comes Home

My CA stopped me mid-transfer: 'Which account are you paying from?' I said NRO. He said: sit down. The account you use to buy Indian property determines how easily you can repatriate the proceeds when you eventually sell. Most NRIs learn this too late.